Starting your first salary? A practical savings framework that actually sticks.

Building savings momentum is easier when goals are tied to specific outcomes like rent buffer or emergency expenses.

Automated transfers, spending caps, and periodic check-ins can turn good intentions into consistent behavior.

Small but steady savings habits usually outperform aggressive plans that are hard to sustain over time.

Splitting income into labeled buckets right after payday reduces the temptation to spend what should be reserved.

Emergency funds should cover at least three months of essentials before chasing aggressive investment returns.

Side-hustle income benefits from its own savings rule so lifestyle inflation does not consume every extra dollar.

Annual subscription charges are easier to absorb when a sinking fund accrues monthly instead of hitting all at once.

Peer accountability—sharing goals with a trusted friend—raises follow-through without needing expensive coaching.

Reviewing progress every quarter lets you adjust targets after real life events like moves or job changes.

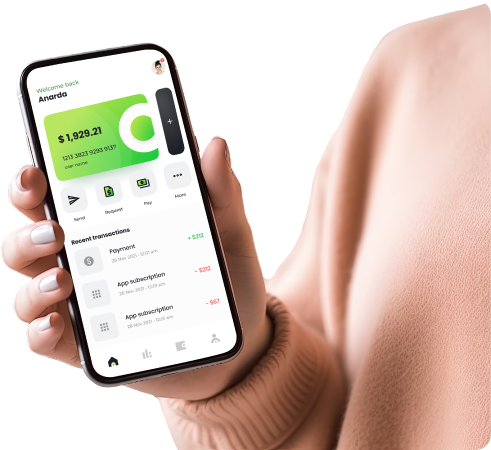

From a saving & budgeting perspective, this update highlights how customers can make better decisions with clearer tools, stronger visibility, and more predictable outcomes.

Looking ahead, KitBank will continue refining this area with user feedback, measured rollouts, and practical education so both individuals and businesses can confidently adopt each improvement.